Fraud Detected: What to Do Next to Protect Your Business

SHARE

Fraud is often hidden in plain sight—until it’s too late. A trusted employee manipulates financial records. A vendor inflates invoices. Funds quietly disappear. By the time the fraud is discovered, the damage is already done.

According to the Association of Certified Fraud Examiners (ACFE) Occupational Fraud 2024: A Report to the Nations®, businesses lose an estimated 5% of their annual revenue to fraud—and in most cases, the fraud goes undetected for over a year.

If you suspect fraud within your organization, acting fast is critical. The longer it continues, the more it costs. But what steps should you take? How do you confirm your suspicions without tipping off the fraudster?

Let’s break down the warning signs, response strategies, and how to prevent fraud before it starts.

The Why

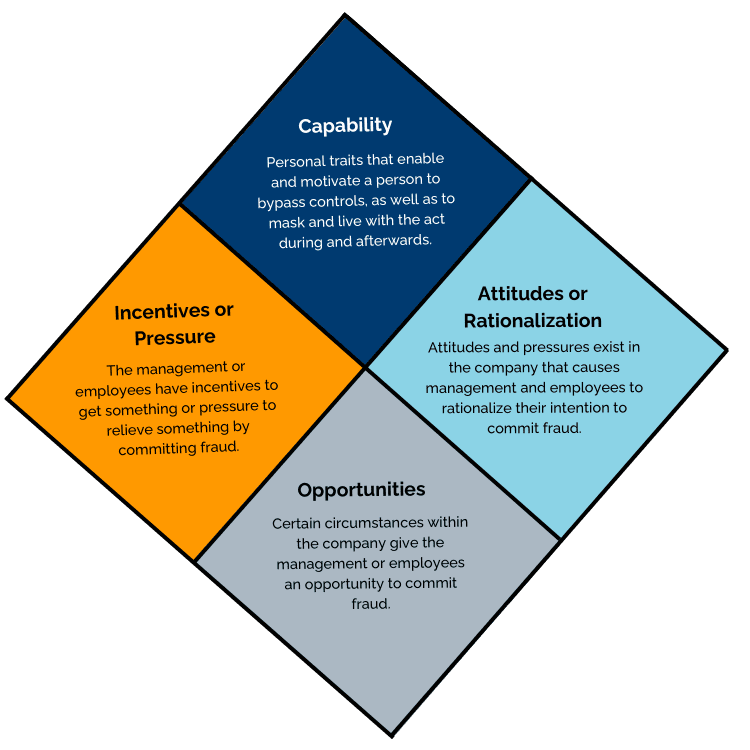

Understanding Why Fraud Happens

Fraud doesn’t happen in a vacuum—it’s often driven by a combination of factors. The Fraud Diamond Theory, developed by David T. Wolfe and Dana R. Hermanson, identifies four key elements that contribute to fraudulent behavior:

Incentives or Pressure – Financial struggles, unrealistic sales targets, or personal debts can create pressure to commit fraud.

Opportunities – Weak internal controls or a lack of oversight can provide the perfect opening.

Rationalization – Employees may justify fraud as a temporary fix or believe they are entitled to extra compensation.

Capability – Some individuals have the skills and confidence to bypass controls without raising suspicion.

Understanding these drivers allows businesses to be more proactive in preventing fraud before it happens. By knowing your key personnel, identifying risky incentives, and strengthening internal controls, you can reduce the likelihood of fraudulent activities.

“The number one cause of fraud is people.” – David T. Wolfe

Red Flags

The first red flags that might indicate potential fraud includes whistle blowers and gut feelings. When someone has too much duty and is able to have control over several financial functions that is a big, red flag.

You might notice one or more of these additional red flags:

Unusual financial transactions, discrepancies in accounts, or missing documentation.

An employee refusing to take vacations (which could indicate fear of being caught)..

Behavioral signs, such as an employee living beyond their means.

To validate your concerns, consider these steps:

✅ Engage an independent advisor – An external professional can provide unbiased oversight. ✅ Conduct an annual fraud risk assessment – Test financial inflows, outflows, and invoices for irregularities. ✅ Strengthen financial oversight – Ensure no single person has complete control over financial processes. ✅ Implement robust internal controls – Segregate financial duties to reduce fraud risks.

Fraud Has Been Identified—Now What?

If you uncover fraud or suspect wrongdoing, follow these immediate steps:

Document Everything – Keep detailed records of suspicious activities.

Consult Your Advisors – Engage a forensic accountant or attorney to assess the financial impact and legal implications.

Isolate the Problem – Restrict access to compromised accounts or processes to prevent further losses.

Involve Legal Counsel – Seek legal guidance before taking action against employees or reporting to authorities.

Additionally, consider annual audits and proactive risk assessments to prevent future fraud incidents. Having a trusted team—CPA, wealth advisor, attorney—can help safeguard your business long-term.

How LGA Can Help

At LGA, we take fraud investigations seriously. Our team works closely with clients to:

✔ Conduct in-depth forensic accounting investigations. ✔ Provide clear documentation of findings. ✔ Coordinate with legal teams to ensure proper reporting. ✔ Assist with litigation and financial recovery efforts.

Whether you’re navigating litigation or seeking recovery from fraudulent activities, we delve deep into fund flows and asset misappropriation while providing litigation support. Our approach focuses on detailed transaction analysis, seamlessly integrating micro-level scrutiny with a macro viewpoint.

Fraud can feel overwhelming, but you don’t have to navigate it alone. If you suspect fraudulent activity, contact us today for a confidential consultation.